LKQ has been treading water for the past six months, recording a small return of 2.3% while holding steady at $41.06.

Is there a buying opportunity in LKQ, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We're swiping left on LKQ for now. Here are three reasons why you should be careful with LKQ and a stock we'd rather own.

Why Do We Think LKQ Will Underperform?

A global distributor of vehicle parts and accessories, LKQ (NASDAQ:LKQ) offers its customers a comprehensive selection of high-quality, affordably priced automobile products.

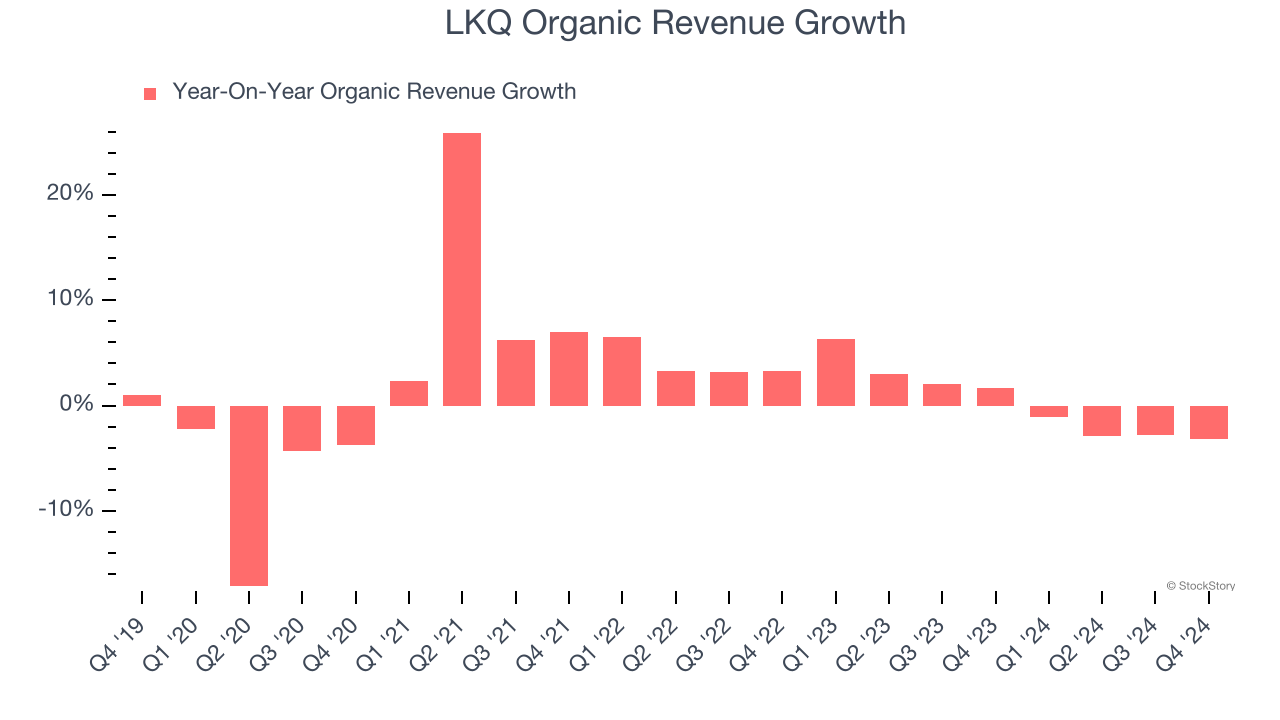

1. Core Business Falling Behind as Demand Plateaus

Investors interested in Specialized Consumer Services companies should track organic revenue in addition to reported revenue. This metric gives visibility into LKQ’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, LKQ failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests LKQ might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect LKQ’s revenue to stall, a deceleration versus its 5.9% annualized growth for the past two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

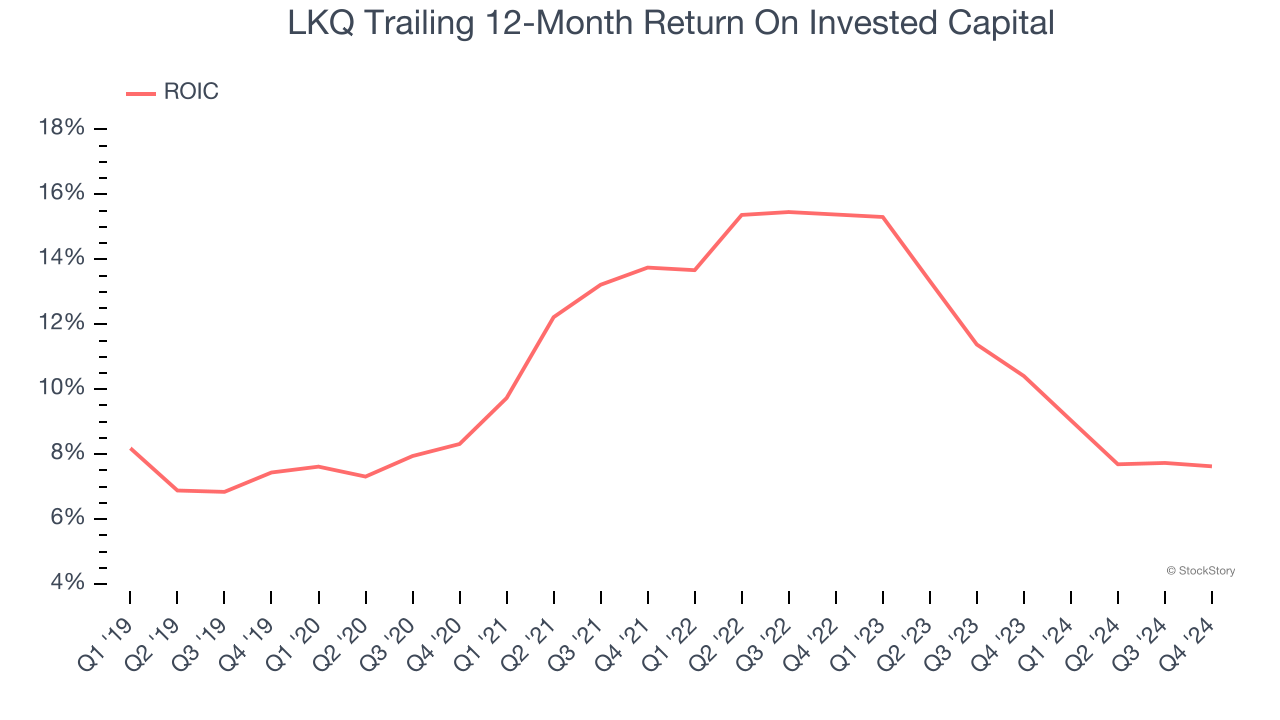

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

LKQ historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 11.1%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of LKQ, we’ll be cheering from the sidelines. That said, the stock currently trades at 11.4× forward price-to-earnings (or $41.06 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than LKQ

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.